categoryUnderstanding Fees

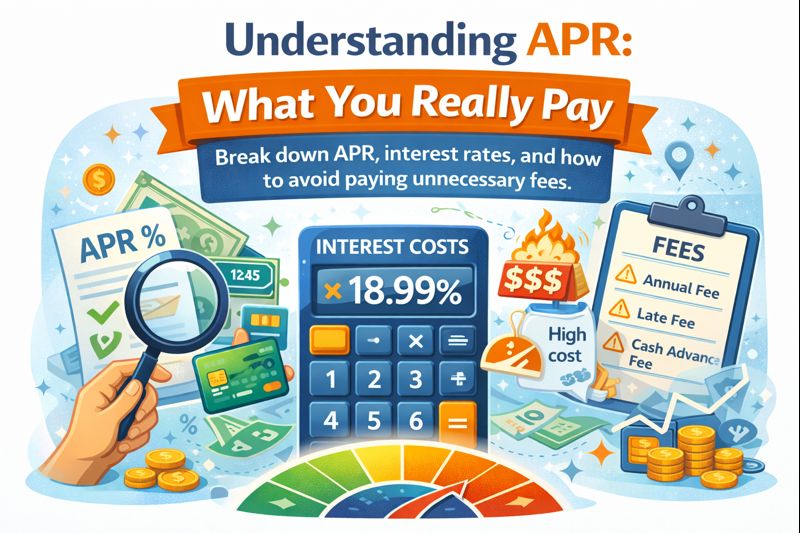

Understanding APR: What You Really Pay

Break down APR, interest rates, and how to avoid paying unnecessary fees.

Break down APR, interest rates, and how to avoid paying unnecessary fees.

When choosing a credit card or loan, you'll almost always see one number highlighted: APR. While it may look like just another percentage, APR has a big impact on how much you actually pay over time — especially if you carry a balance. At HelloBetterCredit.com, we believe understanding APR is essential to using credit wisely. This guide breaks down what APR really means, how it works, and how to avoid paying more interest than necessary.

APR stands for Annual Percentage Rate. It represents the true yearly cost of borrowing money, including interest and, in some cases, certain fees. In simple terms: APR = the price you pay for borrowing money. If you carry a balance on your credit card or loan, APR determines how much interest you'll owe.

Many people use these terms interchangeably, but they're not exactly the same.

Interest Rate: The cost of borrowing the money itself

APR: The interest rate plus certain fees, shown as a yearly percentage

For credit cards, APR typically reflects the interest rate you'll be charged if you don't pay your balance in full

Credit cards often have multiple APRs, depending on how you use the card.

Purchase APR: This is the interest charged on everyday purchases if you carry a balance

Introductory APR: Some cards offer 0% APR for a limited time, usually 6–18 months. Once the intro period ends, the regular APR applies

Balance Transfer APR: Applies when you move debt from one card to another. Often comes with a promotional rate and a transfer fee

Cash Advance APR: Usually much higher than purchase APR — and interest starts accruing immediately

Penalty APR: Triggered by late payments or violations of card terms. This can be extremely high and hard to reverse

Credit card APR is usually variable, meaning it can change based on the prime rate. Here's how interest typically works:

Your APR is divided by 365 to get a daily rate

Interest is calculated daily based on your balance

Interest compounds over time if balances aren't paid off

That's why even small balances can grow quickly if left unpaid

Let's look at a simple example: Balance: $1,000, APR: 20%. Paying only the minimum: You could pay hundreds of dollars in interest over time. APR doesn't matter much if you pay your balance in full each month — but it matters a lot if you don't.

Follow these strategies to minimize interest charges:

Pay Your Balance in Full: This is the easiest way to avoid interest altogether

Take Advantage of Grace Periods: Most credit cards offer a grace period where no interest is charged if you pay in full by the due date

Use 0% APR Offers Wisely: Intro APRs can be powerful — just make sure to pay off the balance before the promo ends

Avoid Cash Advances: They come with high APRs and no grace period

Make More Than the Minimum Payment: Paying extra reduces how much interest accrues

Not necessarily. While a lower APR is helpful if you carry a balance, you should also consider:

Annual fees

Rewards and benefits

Penalty APR rules

Your ability to pay balances in full

If you always pay on time and in full, APR becomes far less important than rewards or perks

Compare 200+ credit cards and find the one that matches your needs and goals.

Browse All Cardsarrow_forward