categoryCredit Score

Credit Score Explained: What It Is and Why It Matters

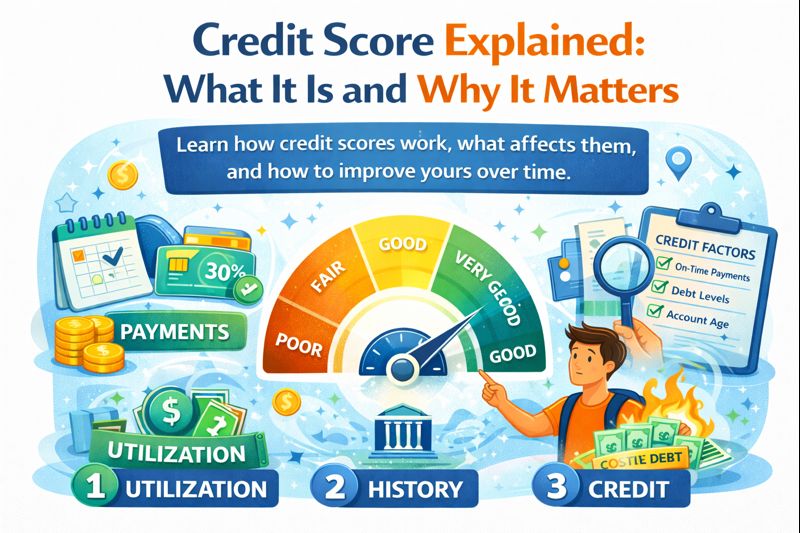

Learn how credit scores work, what affects them, and how to improve yours over time.

Learn how credit scores work, what affects them, and how to improve yours over time.

Your credit score is one of the most important numbers in your financial life — yet many people don't fully understand how it works or why it matters. Whether you're applying for a credit card, loan, apartment, or even certain jobs, your credit score can play a major role. At HelloBetterCredit.com, we're here to simplify credit so you can make confident financial decisions. Let's break it down.

A credit score is a three-digit number that represents how trustworthy you are as a borrower. Lenders use it to estimate the likelihood that you'll repay borrowed money on time. Most scores range from 300 to 850, with higher scores indicating lower risk.

Understanding where you stand:

300–579: Poor

580–669: Fair

670–739: Good

740–799: Very Good

800–850: Excellent

The higher your score, the better your chances of approval — and the lower your interest rates

Five key factors determine your credit score:

Payment History (Most Important): Paying bills on time has the biggest impact

Credit Utilization: How much of your available credit you're using (lower is better)

Length of Credit History: Older accounts help increase your score

Credit Mix: Managing different types of credit responsibly can help

New Credit Inquiries: Too many applications in a short period can lower your score

A strong credit score can help you:

Qualify for better credit cards

Secure lower interest rates

Save money on loans

Get approved faster

Improve financial flexibility

A lower score can limit options and increase borrowing costs

Take these actionable steps:

Pay all bills on time

Keep balances below 30% of your limit

Check your credit report for errors

Avoid unnecessary credit applications

Keep older accounts open

Small, consistent actions can lead to meaningful improvements

Timeline for improvement:

30–60 days: Small improvements from reduced balances

3–6 months: Noticeable progress with good habits

12+ months: Strong, stable credit profile

Patience and consistency are key

Don't believe these misconceptions:

Checking your own credit hurts your score (FALSE)

You need to carry a balance to build credit (FALSE)

Closing old cards always helps (FALSE)

High income means a high credit score (FALSE)

Understanding the truth helps you avoid costly mistakes

Tracking your credit score helps you:

Spot fraud early

Measure progress

Stay motivated

Most tools allow you to check your score without impacting it

Compare 200+ credit cards and find the one that matches your needs and goals.

Browse All Cardsarrow_forward